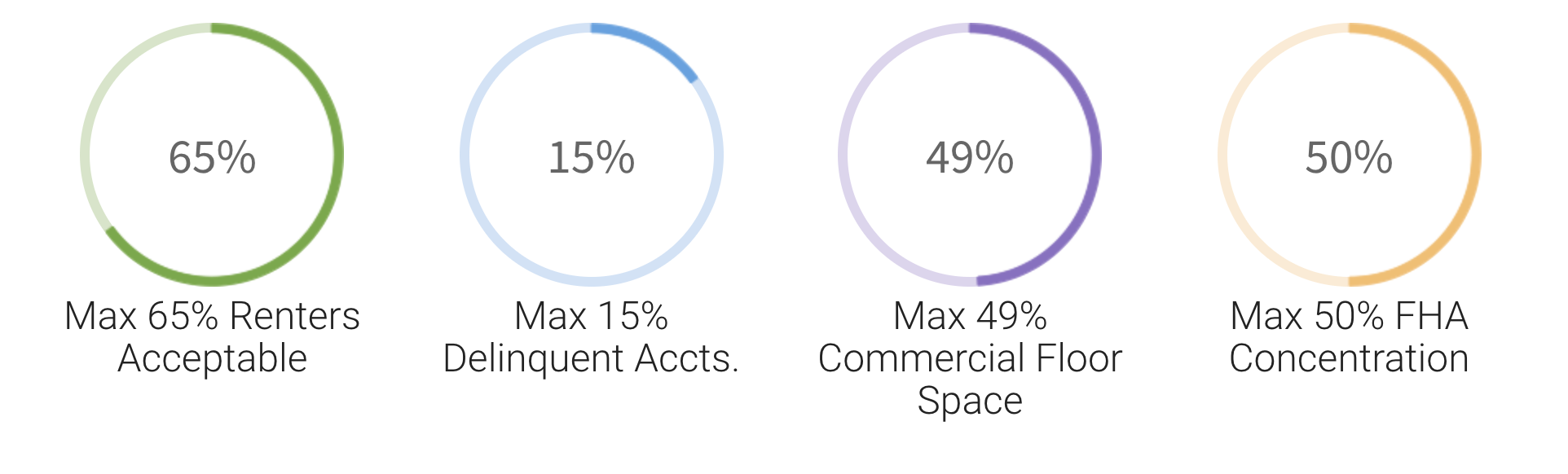

10/26/2016 update – There is an exception to this rule, which reduces the required owner occupancy to 35% (so up to 65% can be rentals). A special set of additional guidelines will apply. Condo complexes with at least 3 years of very stable finances, low delinquency rates, and an up-to-date Reserve Study may qualify for this exception.

recent reserve study)

Assignment of Rents – A requirement that rental income will be assigned to the association if the

unit owner is delinquent in the payment of assessments:

There are different FHA Condo Approval guidelines for 2-4 unit communities. Many times these smaller communities do not have shared expenses, or have very few. Communities without shared expenses typically do not have a community bank account, a budget, or any financial reports, so the FHA will offer an alternative known as a “Memorandum of Understanding.”

A Memorandum of Understanding establishes the responsibilities and maintenance obligations of

each unit owner. Each owner will need to sign and record the memorandum with the County. An

in-state attorney should prepare the Memorandum of Understanding. The cost is usually $200-$500

depending on the size of the community and the attorney.

By providing this document, the association no longer needs to provide financial reports, or comply

with reserve requirements. With this document, they will meet the FHA Condo Approval guidelines.

New Construction also has its own FHA Condo Approval Guidelines. To gain FHA approval for a project that is still under construction, recently converted, or less than 12 months old, a special set of guidelines will apply.

The Developer will need to pre-sell, or have under contract, at least 30% of the units in Phase 1 to become FHA Condo Approved. If a project does not meet this requirement, we cannot continue.

Older condominiums require a list of 10 documents to become FHA Approved. New and Under-Construction projects require a significant amount of additional documentation. These include environmental reports, site photographs, and permits.

The fee for a new construction project is $1,500 in total. This is nonrefundable, but we will work with the project until it becomes approved.

Step 1

The Property Manager or Board Member completes our Eligibility Questionnaire. Our team reviews it to check if it meets the the FHA Condo Approval Guidelines.

Step 2

Our team reviews your application for issues that might conflict with the FHA Condo Approval Guidelines and recommend fixes that help your community get approved.

Step 3

Our team builds and submits your application to the FHA for approval on your behalf. The process takes 2-3 weeks and once approved, your certificate will be sent directly to you!